#23 How Defensive Sectors React When Credit Spreads Widen

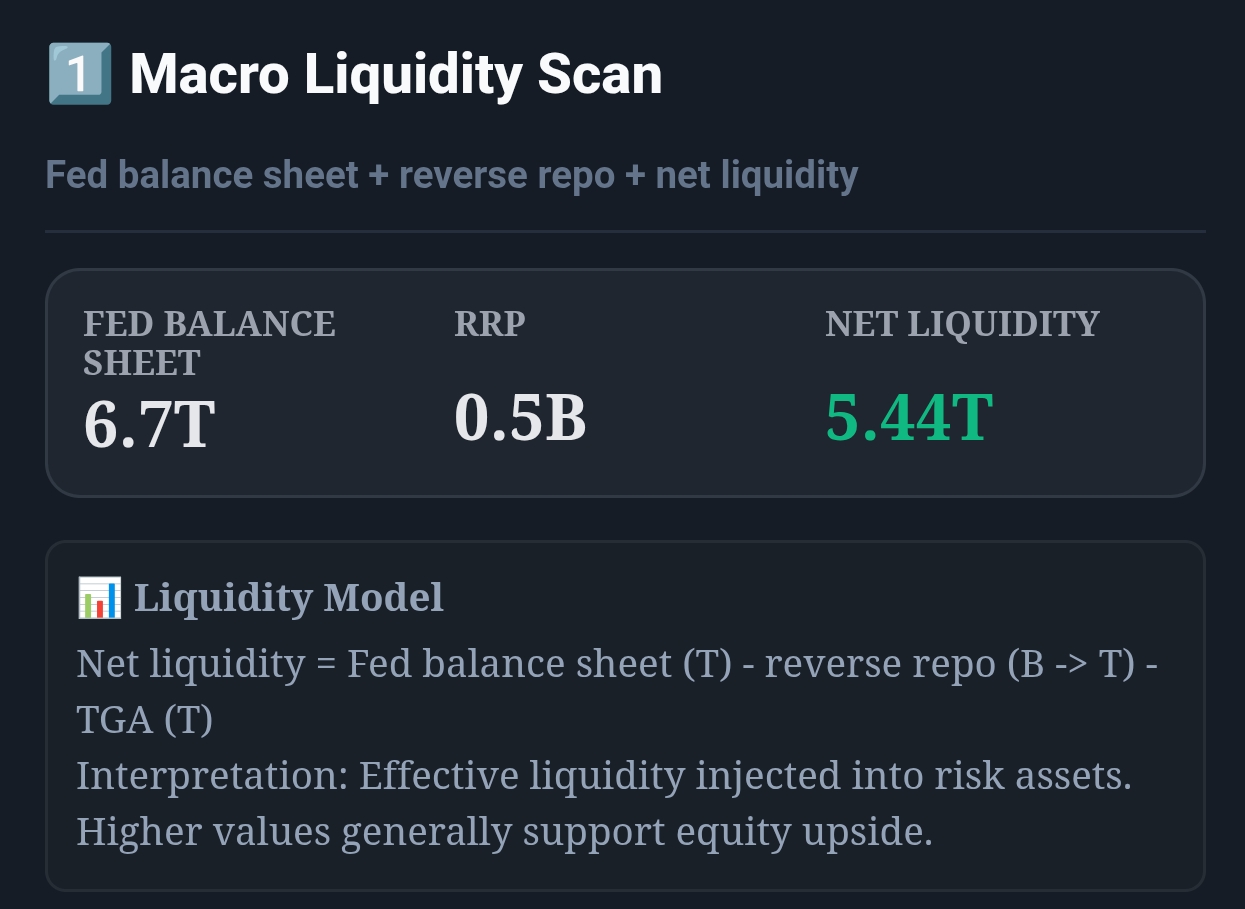

Live capture of Macro Liquidity Scan in Inveflo.

0) Where to Find This Widget

Open the Macro Liquidity Investment System page to access Credit Stress Monitor.

Open /ai-analysis-3.html and find 2️⃣ Credit Stress Monitor. Use its live HY OAS reading as the trigger input for the defensive rotation rules in this guide.

1) TL;DR

When HY OAS widens past 350bp, rotate 20–30% of growth exposure into defensive ETFs (XLU, XLV, XLP). When it crosses 450bp, rotate 40–50%. Utilities, Healthcare, and Consumer Staples outperform by 12–18% on average during credit stress events. The rotation signal leads equity drawdowns by 2–3 weeks.

2) Hook (Pain-Driven)

In Q4 2022, I watched HY OAS climb from 330bp to 520bp over six weeks. I was fully invested in QQQ and XLK. By the time I noticed the damage, QQQ was down 22%. Meanwhile, XLU (Utilities) was down only 3% and XLV (Healthcare) was flat. I had the credit data in front of me the whole time — I just didn't know which sectors to rotate into, or when.

3) Problem

When credit spreads widen, most investors think "sell everything." But that's wrong — and often too late. The real move is sector rotation: moving from high-beta growth sectors (Technology, Consumer Discretionary) into low-beta defensive sectors before equities correct. The challenge is knowing which defensives to buy, in what sequence, and at what credit spread levels.

4) Solution (Widget Introduction)

The Credit Stress Monitor provides real-time HY OAS readings, giving you the trigger levels for defensive rotation. Combine that signal with sector relative strength (XLU/XLV/XLP) to confirm defensives are already starting to lead before you rotate.

Defensive sectors ranked by credit stress outperformance:

- XLU (Utilities) — Tier 1 Defensive: Highest inverse correlation to HY OAS. Stable cash flows, regulated pricing. First to rotate into when spreads widen.

- XLV (Healthcare) — Tier 1 Defensive: Non-cyclical demand, pricing power. Strong in recessionary environments.

- XLP (Consumer Staples) — Tier 2 Defensive: Steady but slightly cyclical. Food, beverages, household products — demand doesn't disappear in downturns.

- XLRE (Real Estate) — Conditional Defensive: Only defensive when credit stress is spread-driven (not rate-driven). Avoid if 10Y yields are also rising.

5) Logic Breakdown (Formula + Thresholds)

Formula: Defensive Rotation Score

DefRotScore = (HY_OAS_level × 0.40) + (HY_OAS_4wk_change × 0.35) + (Sector_RelStrength × 0.25)

- HY_OAS_level: Current spread in basis points. Above 350bp = warning. Above 450bp = crisis.

- HY_OAS_4wk_change: Change in HY OAS over past 4 weeks. Rising >80bp = accelerating stress.

- Sector_RelStrength: Relative performance of defensive sector vs. SPY over past 4 weeks. Positive = defensive already outperforming (confirm rotation).

Thresholds: Rotation Levels by HY OAS

| HY OAS Level | Credit Signal | Growth Exposure | Defensive Allocation |

|---|---|---|---|

| < 300bp | 🟢 Calm | 70% (QQQ, XLK, XLY) | 0% — no defensive needed |

| 300–350bp | 🟡 Watch | 60% | 10% XLV — light healthcare hedge |

| 350–450bp | 🟠 Rotate | 45% | 25% (XLU 10% + XLV 10% + XLP 5%) |

| > 450bp | 🔴 Full Defensive | 20% | 45% (XLU 20% + XLV 15% + XLP 10%) |

6) Practical Use (IF X → THEN Y)

Scenario 1: HY OAS Rises from 310bp to 380bp in 3 Weeks

- Signal: Moderate spread widening. Stress is building but not crisis-level yet.

- Action: Reduce QQQ/XLK by 20%. Allocate 10% into XLV, 10% into XLU. Hold XLP as a next step if spreads continue rising.

- Confirmation: Check if XLU and XLV are already outperforming SPY over the last 2 weeks. If yes — the rotation thesis is confirmed. If no — wait one more week.

Scenario 2: HY OAS Spikes from 360bp to 490bp in 10 Days

- Signal: Acute credit stress. Systemic risk building. Equities will follow within 2 weeks.

- Action: Immediate rotation to full defensive. Cut growth (QQQ, XLK, XLY) by 50%. Allocate 20% XLU, 15% XLV, 10% XLP. Raise 5% cash.

- Horizon: Hold defensive allocation until HY OAS stabilizes and starts falling for 2 consecutive weeks.

Scenario 3: HY OAS at 480bp, Starts Falling to 420bp over 2 Weeks

- Signal: Credit stress easing. Rally setup forming in equities.

- Action: Begin unwinding defensive positions. Sell XLU first (most rate-sensitive). Keep XLV longer (healthcare stays defensive through early recovery). Start rebuilding QQQ/XLK by 15%.

- Risk: Watch for a "head fake" — HY OAS sometimes dips 30bp then reverses. Wait for 2 weeks of consecutive decline before aggressive rotation back into growth.

7) Common Mistakes

Mistake #1: Rotating into Defensives After Equities Already Drop

The point of this strategy is to rotate 2–3 weeks before equities correct. If you wait for SPY to fall 8% before moving into XLU, you've already absorbed half the damage. Use credit spread data as the leading signal — not equity price action.

Mistake #2: Buying XLRE During Rate-Driven Stress

Real estate looks "defensive" on paper (non-cyclical cash flows), but REITs are highly rate-sensitive. If spreads are widening because rates are rising (not because of credit quality deterioration), XLRE will sell off alongside equities. Always check why spreads are widening before including XLRE.

Mistake #3: Ignoring Relative Strength Confirmation

Credit spreads can widen for 1–2 weeks before defensive sectors start outperforming. If you rotate into XLU when it's still lagging SPY, you're paying up for a sector that hasn't confirmed its defensive role yet. Wait for at least 1 week of positive relative strength before adding.

Mistake #4: Staying in Defensives Too Long After Spreads Peak

Defensive sectors underperform massively during the early recovery phase. When HY OAS peaks and starts compressing, growth sectors (QQQ, XLK) begin their strongest rallies. If you stay in XLU through the recovery, you'll miss 15–25% of the growth rebound.

Q: Should I use sector ETFs or individual defensive stocks?

ETFs are strongly preferred for this strategy. Sector ETFs (XLU, XLV, XLP) give you diversified exposure without single-stock risk. Individual defensives can underperform their sector if they have company-specific issues. Use ETFs to capture the sector rotation cleanly.

Q: What about XLI (Industrials) as a defensive?

XLI is not a defensive sector during credit stress. Industrials are cyclical — they often sell off alongside Technology and Consumer Discretionary when credit tightens. Stick to XLU, XLV, and XLP for credit-stress-driven defensive rotation.

Q: How quickly should I execute the rotation?

Over 1–2 trading days. Don't try to time intraday prices. The credit spread signal gives you a 2–3 week lead time before equities correct — so taking 2 days to rotate is fine. Splitting into 2–3 tranches reduces the risk of rotating into a brief counter-trend rally.

Q: Can I use options on XLU/XLV instead of buying the ETFs?

Yes — buying call options on XLU or XLV when HY OAS crosses 350bp is a capital-efficient hedge. A 30-delta call 2–3 months out gives you upside exposure to the defensive rally while capping your downside to the premium paid. Useful if you don't want to fully unwind growth positions.

CTA: Open Macro Liquidity System

Use the live macro, credit, regime, and momentum widgets to validate the rules from this guide.